Nebraska sits in one of the most active hail corridors in the United States. From April through September, storms roll across Lancaster County and can drop golf ball-sized hail on a roof that was perfectly fine the day before. When that happens, most homeowners face the same set of questions: Does my insurance cover this? How do I start a claim? Will I actually get a fair payout?

It covers how a roof insurance claims work from the first phone call through final payment, what insurance adjusters look for, and where most homeowners leave money on the table.

Key Findings

1. Most standard homeowners policies in Nebraska cover hail and wind damage, but they may pay ACV (actual cash value) rather than RCV (replacement cost value), depending on your roof age.

2. Calling a roofer before your insurer is often the smarter move. A written damage assessment gives you a stronger starting point for your claim.

3. Nebraska law gives homeowners the right to get a second estimate if you disagree with the adjuster’s findings.

4. Insurance companies routinely deny claims on roofs over 20 years old, citing wear and tear exclusions. Age of roof directly affects your payout. 5. You have one year from the date of loss in Nebraska to file a storm damage claim.

Why Nebraska Homeowners File More Roof Claims Than Most States

According to the National Weather Service, Nebraska ranks in the top 10 states nationally for hail frequency. Lincoln, Omaha, and the surrounding areas see multiple significant hail events every year, many producing stones large enough to crack shingles, dent gutters, and compromise flashing in a single storm.

Beyond hail, Nebraska roofs also deal with straight-line wind events, ice dams in winter, and temperature swings that accelerate shingle aging. Any of these can trigger a covered claim, depending on your policy.

The challenge is that damage is not always obvious from the ground. A roof can look fine after a storm and still have dozens of impact points that will lead to leaks in the next 12 to 18 months. This is why a post-storm inspection matters before you assume everything is fine.

The Roof Insurance Claims Process: Step by Step

Understanding the sequence of events helps you avoid the common mistakes that slow down or reduce your payout.

Step 1: Get a Roof Inspection First

Before you call your insurance company, get a written inspection from a licensed roofing contractor. A qualified roofer will document every impact point, photograph the damage, and give you a repair or replacement estimate. This report becomes your evidence when the adjuster arrives.

Skipping this step leaves you relying entirely on what the adjuster finds, and adjusters work for the insurance company.

Step 2: File Your Claim

Once you have a damage report, contact your insurer to open a claim. You will be assigned a claim number and an adjuster. Keep every email and record every phone call with dates. This paper trail protects you if there is a dispute later.

In Nebraska, your insurer is required to acknowledge your claim within 10 business days and resolve it within 45 days of receiving your proof of loss.

Step 3: The Adjuster Inspection

The insurance adjuster will schedule a visit to inspect your roof. You have the right to have your roofing contractor present during this inspection. This is important. Adjusters can miss damage, especially on lower-slope sections or behind flashing. Your contractor can point out everything documented in the original assessment.

The adjuster will measure the roof and assess the damage to produce what is called a scope of loss. This document lists what the insurance company agrees to pay for.

Step 4: Review the Settlement Offer

After the inspection, the insurance company sends you an Explanation of Benefits showing what they will cover and how much. Review this carefully against your contractor’s estimate. Common areas where coverage falls short include:

- Code upgrade costs if current building codes require better materials than what was removed

- Matching siding and trim that was not directly hit but no longer matches repaired sections

- Full replacement versus patch repairs on severely aged shingles

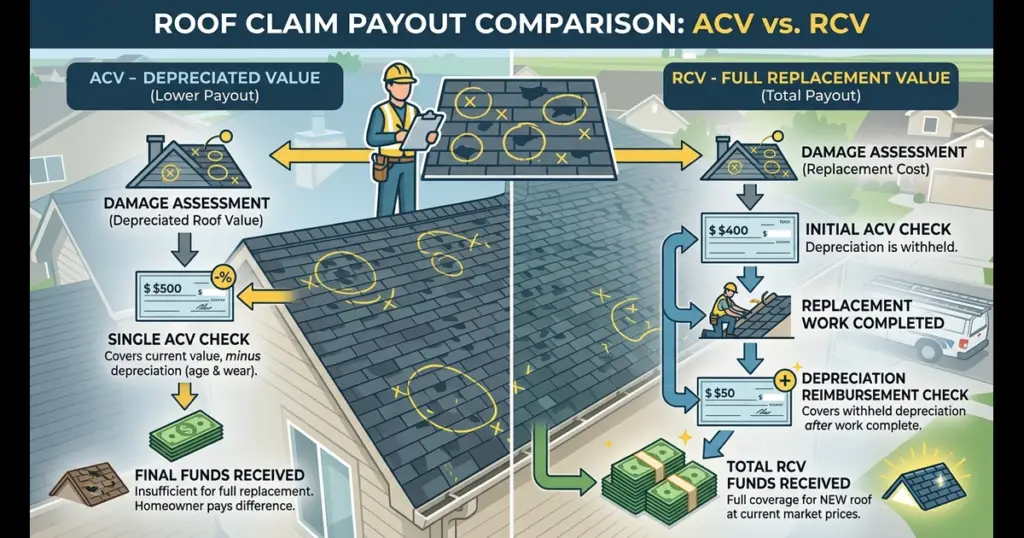

Step 5: Recoverable Depreciation

If you have RCV coverage, your insurer pays the claim in two stages. The first check covers the ACV what your roof is worth today accounting for its age. Once the work is complete, you can file a supplemental claim to recover the withheld depreciation. This second payment can be several thousand dollars. Many homeowners do not know it exists and never collect it.

ACV Versus RCV: The Policy Detail That Changes Your Payout

The single biggest factor in how much you receive from a roof insurance claim is whether your policy covers Actual Cash Value (ACV) or Replacement Cost Value (RCV).

| Policy Type | What It Means for Your Claim |

| Actual Cash Value (ACV) | Pays for a new roof minus depreciation based on the current age of your roof. A 15-year-old roof on a 25-year shingle system might receive only 40 cents on the dollar. |

| Replacement Cost Value (RCV) | Pays the full cost to replace your roof with materials of similar kind and quality, regardless of age. Initial payment is the ACV; remaining depreciation is released after work is complete. |

| Which one do you have? | Check your policy declarations page. Look for “Loss Settlement” or “Roof Payment” schedule. If it lists a depreciation table or “ACV only,” you have ACV coverage. |

If you have ACV coverage on an older roof, your payout may not fully cover the cost of a new roof replacement. This is where our financing options can cover the gap between what insurance pays and what the project costs.

What Insurance Adjusters Look for During a Roof Inspection

Knowing what the adjuster is evaluating helps you prepare. These are the main items they assess:

- Hail impact points on shingles — circular bruising or granule loss concentrated in a pattern

- Wind damage — lifted, curling, or missing shingles along ridges and edges

- Flashing condition around chimneys, skylights, and pipe boots

- Gutter damage — dents on downspouts and gutters are a reliable secondary indicator of hail size

- Roof age and condition — adjusters document pre-existing wear to limit the claim scope

- Interior evidence of water intrusion — attic stains, wet insulation, or ceiling damage inside

Adjusters are trained to distinguish storm damage from wear and tear. Pre-existing granule loss, cracked caulk, or shrinkage are typically excluded from coverage. A roofer who knows what covered damage looks like can ensure nothing legitimate gets categorized as maintenance neglect.

What to Do If Your Claim Is Underpaid or Denied

Insurance disputes are more common than most people expect. Here are the options available to Nebraska homeowners when a claim falls short:

Request a Re-Inspection

If the adjuster missed damage documented in your contractor’s report, ask the insurance company to send a second adjuster. Provide your contractor’s full written report and photos as supporting evidence.

File a Supplemental Claim

If the scope of loss changes after the initial adjustment, for example if the contractor finds additional damage during the actual repair, you can file a supplemental claim to cover the additional work. This is standard practice and insurers are required to review it.

Hire a Public Adjuster

A public adjuster works for you, not your insurance company. They assess the damage independently and negotiate directly with the insurer. Public adjusters typically charge 10 to 15 percent of the final settlement. For large claims, this cost is often justified by the increase in payout.

File a Complaint with the Nebraska Department of Insurance

If your insurer is delaying, lowballing, or acting in bad faith, you can file a complaint with the Nebraska Department of Insurance. This creates an official record and often prompts faster resolution.

Working With a Roofing Contractor Who Knows the Insurance Process

Not every roofing contractor has experience working alongside insurance claims. The difference matters.

A contractor familiar with the claims process will document damage in a format that aligns with how insurance adjusters write scopes. They know how to communicate directly with adjusters, what language to use in supplemental requests, and how to identify recoverable depreciation on your behalf.

What to confirm before hiring a contractor for an insurance job:

- Do they carry valid contractor licensing in Nebraska?

- Will they be present during the adjuster inspection?

- Can they provide a detailed written estimate that matches insurance scope format?

- Do they assist with the depreciation recovery process after the job is complete?

- Are they familiar with current Lincoln building codes for roofing materials?

Integrity Exterior Solutions works directly with homeowners through every stage of the claims process, from the initial storm damage inspection through final supplement collection.

Protect What the Storm Left Behind

Nebraska storms do not wait for a convenient time. A hail event can happen in May and leave damage that does not show as a leak until November. By then, the window to file a claim may be closed.

The most important step after any significant storm is getting a free roof inspection from a licensed contractor before assuming everything is fine. A written inspection report costs you nothing and gives you documentation that protects your claim from the start.

| Schedule a Free Storm Damage Inspection Integrity Exterior Solutions serves Lincoln, NE and surrounding Lancaster County. We inspect your roof, document the damage, and walk you through the claims process at no charge. Call (402) 730-3077 |

FAQs

Q: How do roof insurance claims work in Nebraska?

A: You document damage with a contractor, file a claim with your insurer, meet with an adjuster, review the settlement offer, and collect recoverable depreciation after repairs are complete.

Q: Will insurance cover a 20-year-old roof in Nebraska?

A: It depends on your policy. ACV policies depreciate older roofs, often paying less than full replacement cost. RCV policies cover full replacement cost regardless of age.

Q: How long do I have to file a roof insurance claim in Nebraska?

A: Nebraska homeowners generally have one year from the date of the storm to file a claim, though you should check your individual policy for specific deadlines.

A: Call a roofer first. A written damage inspection report gives you evidence before the adjuster arrives and strengthens your claim from the start.